As we think about investment themes for next year and beyond, one thing that stands out is that there are attractive opportunities in fixed income again for the first time in a long time. The interest rate adjustment that saw the 10-year Treasury jump from a low of just 0.32% in the depths of the pandemic back in March 2020 to a recent high of 5% thanks to the Federal Reserve’s most aggressive rate hiking campaign in decades was certainly uncomfortable for bond holders as it occurred. But as the Fed wraps up this tightening cycle and the dust settles, the fixed income landscape suddenly looks quite interesting again. However, not all bonds are created equal and while traditional treasury and corporate bonds do offer higher yields now, we believe the real opportunities lie in other corners of the bond market. One area in particular that stands out is securitized credit.

Securitized credit refers to bonds that are created from pools of various types of loans – mortgages, auto loans, credit card receivables, corporate bank loans, etc. Wall Street’s finest financial engineers then package hundreds or thousands of them together to create bonds that have different tranches, or slices, of various credit quality. According to some private estimates, this is as large as a $5 trillion market, or more than 3x the size of the corporate high yield market. However, this part of the market is often underrepresented or avoided altogether in most investors’ index or fund holdings that usually focus on treasuries, investment grade corporates, and perhaps municipals. The good news is that it’s increasingly becoming a more accessible area for investors to take advantage of with the launch of newer funds that directly target these securitized bonds.

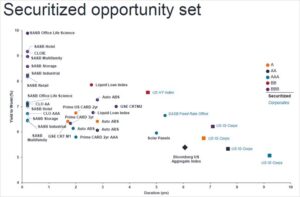

Right now, the opportunity set in securitized credit looks very attractive with even the higher-rated parts of this market advertising yields that are considerably above traditional bonds, and often have shorter maturities and thus less interest rate sensitivity to boot. The chart below highlights this, with various types of securities credit shown by the different colored circles generally clustered together towards the left/upper left side of the chart indicating higher yields (y-axis) and relatively short durations (x-axis). Compare this to the overall Bloomberg Aggregate Bond Index (shown by the black diamond) or traditional corporate bonds (shown by the squares) that are located more towards the lower and right side of the chart, and it becomes clear that securitized credit currently stands out in terms of offering more bang for the buck.

2024 should be a much better year for fixed income investors, especially if the Fed delivers on a few rate cuts that the market is now anticipating. While nearly all bonds should benefit in that scenario, we believe that the starting point for securitized credit of higher relative yields means that they’re positioned to shine even more.

Source: Bloomberg, Janus Henderson, updated quarterly as of 9/30/23

Carl Noble, CFA®

Senior Vice President of Investments

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.